Editor’s note: This year’s World Feed Panorama survey has changed. It has been thoroughly revised and upgraded to take account of more sources from more countries as well as being extended for sectors and to bring in more of the feeds made by mills that are part of integrated production networks.

The decision to look more closely at the integrators was inevitable, given the increasing scale of operations that in the past may have been categorized as farm mixers as well as the strong presence of integrated enterprises among the world’s larger feed manufacturers.

World feed production was remarkably resilient in 2012 despite facing extremely challenging conditions. Many early expectations had been that the total global tonnage of industrially produced compound feeds would show a significant reduction in 2012 under the pressure of high raw-material costs and weak farm market prices. But, the general indication from our latest annual World Feed Panorama survey is that volumes were maintained across a wide range of countries, even if the explanation for this stabilized performance seemed to vary widely from one country to another.

Of course, the downside was that the relative stability meant an absence of overall growth. In this respect, it added to earlier evidence that the expansion of world feed production is slowing after a 15-year history of notable increases.

Slowing increases

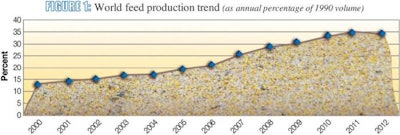

The results of previous World Feed Panorama surveys suggested that global compound feed production grew by about 3.5 percent between 1995 and 2000 and by almost 5.75 percent between 2000 and 2005. The tonnage recorded in 2010 was about 12.25 percent more than in 2005.

On closer examination of the data, however, the most pronounced period of growth for the industry came in the years immediately after 2005, as the accompanying Figure 1 illustrates. Broadly, similar volumes have been added consistently year by year in recent times, but each addition meant a progressively smaller percentage annual increase down to 1 percent.

A standstill year

Even with taking our new revised survey format into account, it seems we should regard 2012 as a standstill year from the viewpoint of the total output of complete diets by industrially sized mills. As national data for 2012 become firmer, they are likely to point to a world market for compounds that can be estimated approximately at 817 million metric tons (Figure 2). Additional data regarding world feed production by species can be found in Figure 3.

Apart from the industrially produced compounds, the modern farm-mix sector conceivably contributes millions of metric tons per year to the overall feed market at a global level. However, the actual size of the sector’s contribution remains highly contentious in the absence of good measurements. The fact that world animal protein production is growing faster than recorded feed output may imply that an increasing number of farmed animals, poultry and fish are receiving farm-produced nutrition.

FEFAC calculations

Within the European Union area, the European Feed Manufacturers’ Federation, FEFAC calculates that compounds from industrial manufacturers supply less than one-third of the 470 million metric tons of feeds needed annually for farm animals in the member states (Figure 4). Canadian estimates say that one-third of all feeds used in Canada are farm-produced.

According to the International Feed Industry Federation, more than one-quarter of all feed supplies worldwide originate from mixing ingredients on the farm.

The FEFAC federation in Europe has reported an almost identical total of 151.9 million metric tons for the feed tonnage of the EU-27 countries in 2012, as in 2011. Its compilation of national results found that overall increases of 1 percent for poultry feeds and 1.5 percent for cattle feeds had compensated for a downturn of 1.9 percent in pig feeds (Figure 5). The changes increased poultry’s slice of the EU feed market to nearly 33.9 percent while cattle’s grew to 26.6 percent, but the share of pig feed fell to under 32.5 percent.

Contrasting trends

See in Figure 6 that the six largest national feed industries in the EU-27 have shown contrasting trends over the last three years. FEFAC noted increases in 2012 of 2.4 percent for the UK and 2.3 percent for Germany, whereas production in France stayed virtually unchanged, and there were production decreases of 0.9 percent for Spain, 1.8 percent for Italy and 2.1 percent for the Netherlands. Outside the top six, Denmark’s output dropped by 200,000 metric tons, or 4.9 percent, due to a cutback in sales of pig feed, reflecting the poor profitability of European pork producers.

Key points

Asia-Pacific remains by far the largest region for world feed market share, including China’s production. In 2012, the region accounted for 33.75 percent of all industrially produced compounds; China alone accounted for 17.4 percent of the tonnage, with other Asia-Pacific countries providing slightly more than 16.3 percent.

Europe with Russia had a 2012 world market share of 22.8 percent, compared with 21.75 percent for North America; Latin America contributed 15.6 percent; and the other 6.4 percent came from the combined tonnages of the Middle East plus Africa.

Almost half the world’s production of compounds in 2012 comprised feeds for poultry (Figure 3); the share of regional tonnage taken by poultry feeds varies from 60-65 percent in the Middle East plus Africa and Latin America, down to 48 percent in Asia-Pacific, 39 percent in North America and 36 percent in Europe with Russia.

Data from this story, together with additional feed data, may be downloaded from www.WATTAgNet.com/marketdata/feed/